Florida Insurers Have Paid Just Half of Claims From Hurricanes Milton and Helene—Home Insurance CEO Explains Why

RICARDO ARDUENGO/AFP via Getty Images

Home insurance companies in Florida have paid only half of the claims filed in relation to Hurricanes Milton and Helene last fall, leaving some homeowners frustrated—but a top CEO says there is more to that figure than meets the eye.

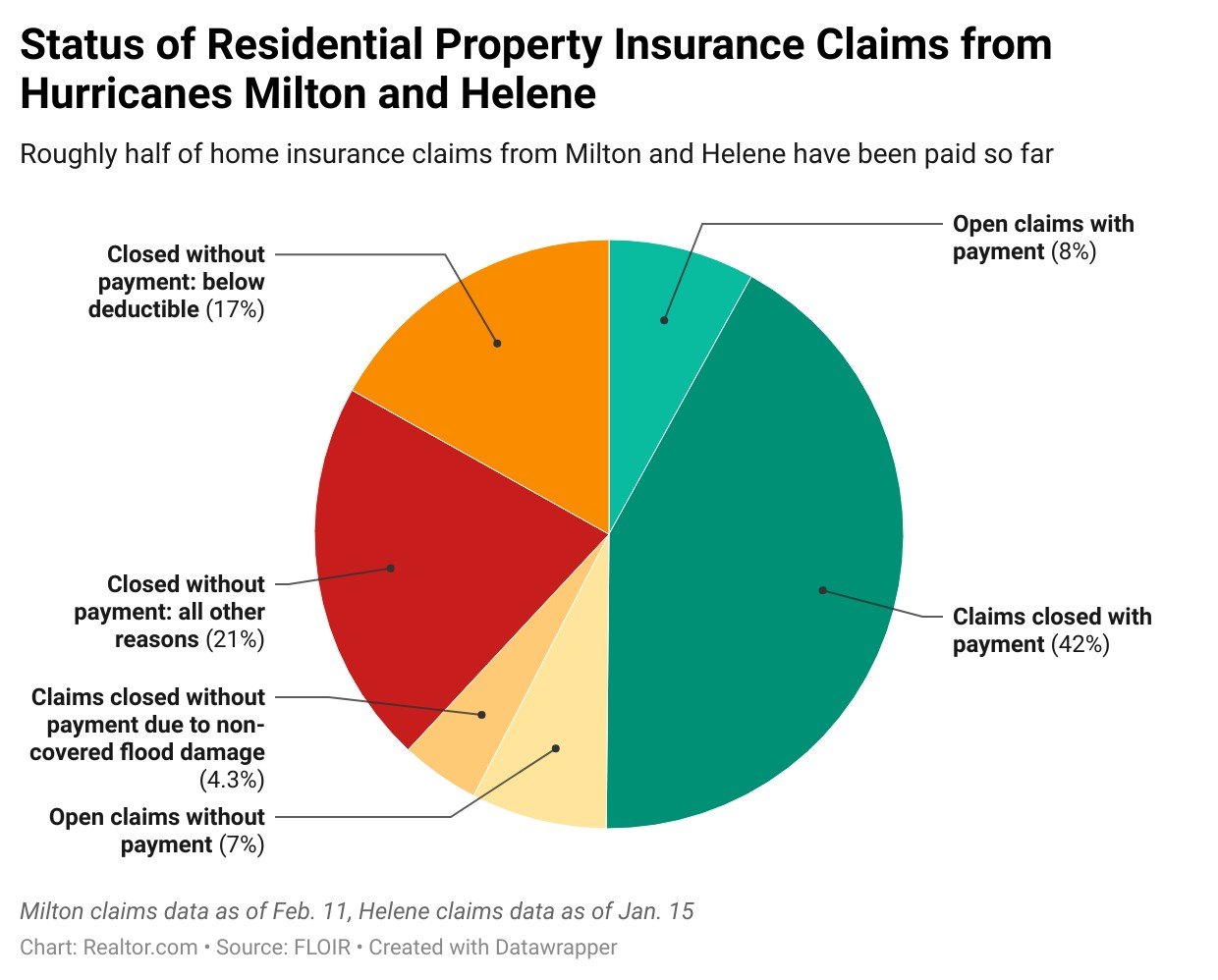

Of the more than 329,000 residential property insurance claims filed in Florida after the two successive storms, 42% were closed without payment and 7% are still open and unpaid, according to the latest data from the Florida Office of Insurance Regulation (FLOIR).

Slightly more than half of the total claims (50.2%) now show as either closed and paid, or open with payment.

Hurricane Helene hit Florida’s Big Bend region on Sept. 26, 2024, as a Category 4, and then went on to cause major inland flooding in parts of Georgia and North Carolina. Less than two weeks later, Milton was at Category 3 when it struck Florida’s Gulf Coast south of Tampa and carved across the state.

In Florida, the storms did much of their damage through high winds, which is covered by traditional homeowners insurance. Both also caused flooding, although that is typically covered separately by a federally administered program, which is not reflected in the state insurance data.

(Getty Images)

Top home insurer explains main reasons for denying claims

Locke Burt, the CEO of one of Florida’s biggest home insurance carriers, Security First Insurance Co., tells Realtor.com® in an extended phone interview that his firm is working to speedily resolve hurricane claims.

Of the roughly 5,000 claims Security First has received in relation to Milton, Burt says about a quarter of the claims have been closed with payment and 15% are open with payment.

Also, 16% are still open without payment, but many of those claims either were filed in the past 30 days or are waiting for a contractor to become available to make the necessary repairs.

Of the remaining claims—a little more than 40% of the total—Burt says about half were closed because the damage was under the homeowners’ deductible.

“The deductibles in Florida are big. The normal hurricane deductible for most people is 2% of the value of the house. So if your house is valued at $400,000, that’s an $8,000 deductible,” he says.

Roughly 1,000 claims, or 20% of the total, were simply declined, typically because the damage reported was not covered under the policy.

Burt says that, in many cases, homeowners file a claim for flood damage fully expecting the claim to be denied, because they must have a denial in hand from their homeowners policy before they seek reimbursement from federal flood insurance.

In other cases, claims are denied because they are for damage to fences, screened porches, or other structures not covered by the insurance policy.

“Another reason that we deny coverage is because there’s a significant number of people in Florida who buy a policy that excludes wind damage, and they forget that their policy excludes wind damage,” says Burt. “It’s not because we’re being bad guys.”

Other, relatively less common, reasons for denial include duplicate submissions, incomplete applications, or claims that are withdrawn by the homeowner for some reason.

(CHANDAN KHANNA/AFP via Getty Images)

Burt also praised Florida for posting insurance claim resolution data online, saying that people have a right to know how claims are being processed and ask questions.

“We have a difficult business to understand,” he says. “But one thing that Florida is doing well is putting all this data together and putting it on the web.”

Overall, according to FLOIR, residential property insurance policies have paid out $2.4 billion in claims related to Milton, and $500 million for Helene.

Excluding federal flood insurance, total payments for the two hurricanes in Florida, including commercial and auto policies, have topped $5.7 billion.

Homeowners express frustration at delays, denials

Still, some homeowners in Florida have expressed frustration at lengthy claims processes or claims that are denied.

Inland flooding around Lakeland’s Lake Bonny caught many homeowners by surprise, as the area is not a FEMA-designated flood risk zone, and many did not carry flood insurance on their homes.

Those who did have flood insurance have also faced frustrations.

Lake Bonny resident Misty Wells told the Lakeland Ledger that her home foundation cracked after sitting underwater for 20 days.

Her flood and homeowners insurance won’t cover the foundation repairs, estimated at $46,000, leaving her unable to proceed with covered repairs to the walls, she says.

“If we have to wait another six months for an answer, we might as well not rebuild until after the summer,” she told the outlet. “Because at least this way, if it floods again, the water can flow right through the house. It ain’t going to damage nothing—it’s already gutted.”

Categories

Recent Posts

"My job is to find and attract mastery-based agents to the office, protect the culture, and make sure everyone is happy! "

1637 Racetrack Rd # 100, Johns, FL, 32259, United States